Insights

A collection of our recent articles, white papers, webinars, reports and videos.

TAS hires Andrew Quartermaine as COO and General Manager of International Business

ASTRO IT joins TAS Group

TAS launches SoftPos to accept contactless payments from Android devices

Thanks to the agreement signed with Danish fintech SoftPay, TAS will enable the acquiring of contactless payments from Android mobile devices in Italy. The benefit provided by the SoftPos solution to merchants is simple and immediate: allowing to transform their phones into a ready-to-use payment terminal, without the need for additional certified hardware, thus reducing the heterogeneity and complexity of multi-device management at the point of sale.

The shopping experience is also improved for the buyer, who can complete the payment faster, avoiding long queues at the checkout.

The merchant APP is available on the Google Play Store and can be used in white label mode, or easily integrated with any APP already in use by the merchant.

The solution is certified with Visa and Mastercard, and is also available for mobile wallets - such as Apple Pay, Google Pay, Samsung Pay - whose payments are processed in a similar way to standard EMV transactions managed by traditional POS devices. For maximum user security, a specific certified component manages the typing of the PIN on Glass on the Android device, ensuring absolute confidentiality.

The SoftPos solution is offered by TAS to banking operators and their processors as a service in Cloud; in this way the impact on the Service Provider is minimal, avoiding to disrupt the infrastructures already in use to manage the POS channel.

Tuscany Region confirms TAS for the evolution of its digital platform IRIS

- administrative and technical enrollment of public bodies belonging to the Tuscany territory

- standardization of interfaces and integration with the national IO App system, with full reconciliation of receipts

- simplification of the payment experience of the users (citizens and businesses)

- integration with regional apps

- integration with the centralized booking system for public healthcare services (CUP) and the Pharmacies of the Tuscan Health Service.

TAS strengthens its tools and offering in terms of cybersecurity

TAS increases the security level of its software thanks to Synopsys’ best in class solutions

Rivean Capital is the new majority shareholder of TAS

ECMS Updates

Interest is growing in the Aquarius User Group initiative, whose last meeting was held on April 20 in Milan, with over 70 participants including representatives of the major financial institutions and service centers committed to meeting the Eurosystem deadlines.

The working group, coordinated by TAS in collaboration with Accenture and KPMG, took stock of the progress of the ECMS project, illustrating the new documentation being released by the ECB and all remaining regulatory milestones impacting on the banking community. A live demo of TAS Aquarius ECMS component was presented, focusing on the monitoring and management fuctionalities designed around the Eurosystem's new unified Collateral Management system. On top of collecting feedback from the first 10 clients that have adopted the new Aquarius module, the meeting was a valuable opportunity to present and discuss additional value-added features that will be provided by Aquarius in order to offer, beyond the full compliance with the new ECMS requirements, also several scalable functions managing further forms of collateral.

An update on the T2-T2S Consolidation project was also part of the meeting agenda, with a deep-dive into the topic of testing, now in its most intense phase, as well as a summary of the upcoming activities defined by the ECB before the Go Live scheduled for 21 November.

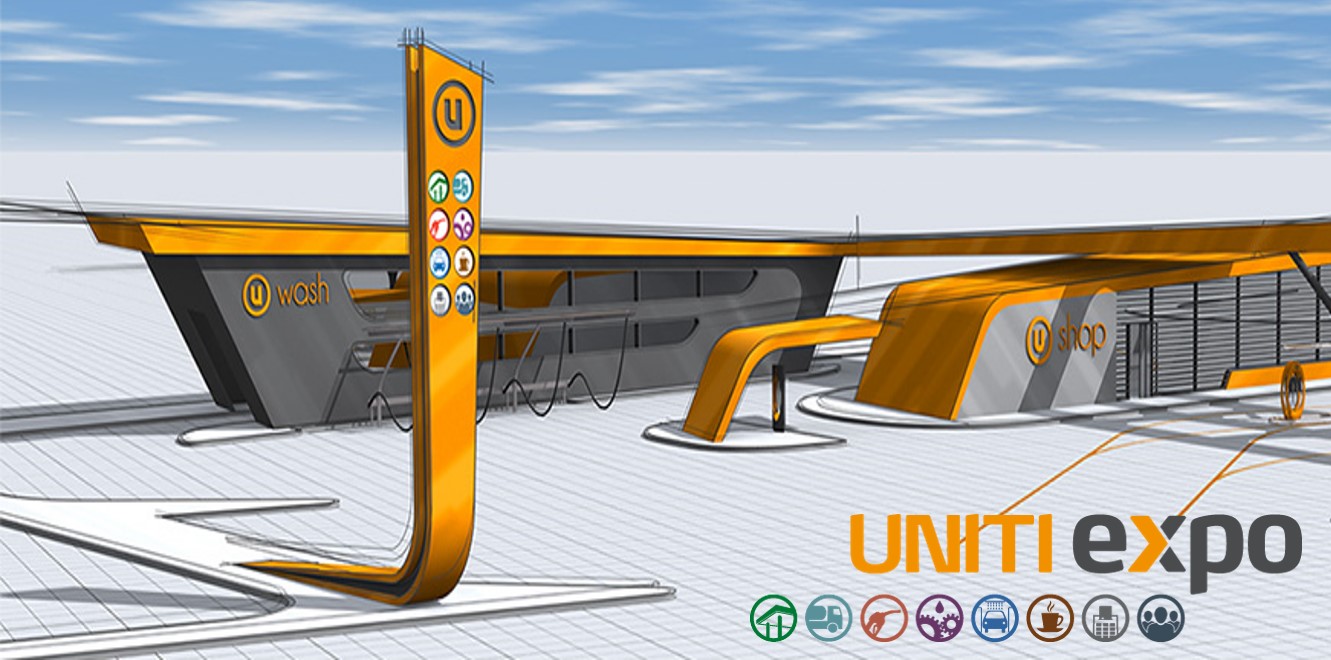

Infraxis showcasing its comprehensive Fuel technology at UNITI EXPO

Lugano, 9 May 2022 – Infraxis AG, part of TAS Group, a leading technology provider in the Payments space, will be exhibiting at the upcoming UNITI EXPO taking place in Stuttgart from May 17 through 19. We’re proud to be at UNITI 2022, where we’ll be co-exhibiting with CCCBusiness Service AG, our processor partner servicing the top forecourt operators and fuel card issuers in Switzerland and beyond.

The state of the art PayStorm Fuel platform is powering CCC business by supporting leading Fuel Industry operators on a daily basis. Infraxis is continually investing in the PayStorm platform, bringing the challenger bank paradigm to the processing of fleet cards, forecourt acquiring and EV charging apps.

PayStorm efficiently solves challenges associated with acquiring and authorizing fuel card payments through its highly adaptable design, enabling the realization of different business needs within the minimum of time and with the minimum of cost.

“Whether your organization needs to acquire internationally branded cards, perform authorisation against a small to medium sized card portfolio, or to simply to switch out to a card issuer for authorisation, Infraxis has the solution ready to satisfy your processing requirements.”- commented Manfred Thomi, CEO of Infraxis.

At the UNITI Expo Infraxis stand visitors will be able to assess the ease of app integration via APIs for mobile-first onboarding and self-management for both fleet cards and international payment brands.

UNITI Expo, the leading retail petroleum and car wash trade fair in Europe, is finally back in-person, with 4 themed exhibiting areas. Infraxis AG welcomes all interested visitors in Hall 5, the Technology, Payment & Logistic area, at booth 5A20.

Contact us

Get in touch to discover how we can help in achieving your business goals