Insights

A collection of our recent articles, white papers, webinars, reports and videos.

ECMS Updates

Interest is growing in the Aquarius User Group initiative, whose last meeting was held on April 20 in Milan, with over 70 participants including representatives of the major financial institutions and service centers committed to meeting the Eurosystem deadlines.

The working group, coordinated by TAS in collaboration with Accenture and KPMG, took stock of the progress of the ECMS project, illustrating the new documentation being released by the ECB and all remaining regulatory milestones impacting on the banking community. A live demo of TAS Aquarius ECMS component was presented, focusing on the monitoring and management fuctionalities designed around the Eurosystem's new unified Collateral Management system. On top of collecting feedback from the first 10 clients that have adopted the new Aquarius module, the meeting was a valuable opportunity to present and discuss additional value-added features that will be provided by Aquarius in order to offer, beyond the full compliance with the new ECMS requirements, also several scalable functions managing further forms of collateral.

An update on the T2-T2S Consolidation project was also part of the meeting agenda, with a deep-dive into the topic of testing, now in its most intense phase, as well as a summary of the upcoming activities defined by the ECB before the Go Live scheduled for 21 November.

How the T2-T2S Consolidation and Instant Payments will affect BCBS248

While the imminent deadline of the T2-T2S Consolidation project together with the SWIFT CBPR+ Project, have absorbed time and resources at the bank’s side, the impact they will have on Intraday liquidity management is also likely to be heavily felt. When BCBS248 was introduced back in 2013, it brought with it a new set of best practices for the monitoring and measuring of intraday liquidity, throwing the topic into sharp focus. Key improvements introduced included a better distribution of payment outflows as well as the re-design of all processes around data acquisition, reconciliation and bilateral agreements with respective correspondent banks. In other words, it was only relatively recently that banks have started assessing their intraday liquidity exposure and adjusted their internal workflows to maintain and optimise their Intraday liquidity buffers.

The first major step that introduced disruption to the bank’s data management was switching from EOD batch processes towards an intraday approach. Whilst real-time and intraday management were long known within RTGS systems, it changed Correspondent Banking relationships considerably, where the banks were used to receiving EOD statements on a daily/weekly basis.

A second major turning point was assessing what systems and what obligations were to be considered for the metrics calculations, generally linked to any ancillary system activity as well as fiscal related payments and CLS. While BCBS248 addresses the basic guidelines to be taken into consideration when calculating metrics, at a general level, much of the implementation is left to the individual bank’s interpretation. The ECB’s current developments and the systems centralisation processes (T2, T2S and TIPS), have opened new user interpretations with regards to what payments flows to include in the metrics calculation. Some banks have opted to include all ECB systems as a whole in their intraday buffer calculations. Other banks report only the RTGS activities and consider all other systems as ‘’ancillaries’’ that work independently for closing their position on the LVPS at the end of day (e.g. EURO1/T2S) without creating intraday liquidity exposures on the RTGS side.

The Basel Committee has been very clear in stating that metrics reporting should be performed on a LVPS system on a system and currency basis. Other LVPSs can be included in the same report provided that liquidity bridges exist with the main LVPS; where ancillary systems are concerned, there’s no need to report them individually as they settle on the LVPS during the selected operational windows.

One of the trends that has being observed during the assessments conducted in the pre T2-T2S Consolidation phase, is that banks are keen to move most of the retail payments towards clearing and/or IP services, reducing the liquidity impacts on the LVPS. As a result, a significant portion of liquidity will no longer be settled in the LVPS, but managed on separate systems/accounts.

With this upcoming new situation, we will be seeing the migration of a big chunk of liquidity toward non-LVPS related systems that are out of scope for the current BCBS248 scenarios.

Instant Payments, as we know, are independent from clearing and settlement mechanisms and don’t close their position on any existing LVPS. That means that they settle continuously and independently; in case of liquidity shortages or surpluses, it is possible to move funds in and out and measure them accordingly in the metrics calculations of the respective LVPS system (backed by collateralised capacity, typically held at the Central Bank).

The participation in the ECB Instant Payment System, TIPS, will become mandatory for all TARGET2 actors from November 2021, to encourage the usage of the platform and driving the change toward alternative and more cost-effective means of payment. Additionally, TIPS will become the main hub for all funding and defunding activities across all IP schemas, making liquidity available at any time through automated processes.

However, from a BCBS248 perspective, it will still be possible to measure funding and defunding transfers made from/to the RTGS system to/from the dedicated cash account in TIPS.

That said, IP statistics indicate a strong growth trend (one that varies across jurisdictions) mostly driven by individual banks expanding their product offerings as well as an acceleration in the digitalisation processes in the Covid era.

IP volumes are getting higher and will most likely replace the normal ACHs in the retail sector. This is not only driven by cost and efficiency benefits, but also to ensure settlement finality for high value payments. In TIPS all retail payments are eligible for settlement in central bank money, regardless of the amount. The general perception is that we will experience a gradual shift from an intraday liquidity monitoring approach towards a fully automated real-time control; liquidity exposures won’t stop overnight but will keep on running 24/7 in different currencies and systems as a result of interoperability initiatives across the globe.

Likewise, SEPA itself has started the migration process towards a Continuous Gross Settlement schema; banks will now be able to settle SEPA payments on a real-time basis but still outside the LVPS settlement windows. Banks have been used to knowing exactly at what time during the day to expect each settlement, while in a continuous gross settlement environment, batches will be settled on separate technical accounts where liquidity needs to be available at selected ‘’intervals’’ if needed.

Tracking what used to be considered as a ‘’timed obligation’’ on an intraday basis is now opening different views and interpretations. Unless formally stated as part of a regulatory update, the reporting of IP activities and SEPA Continuous Gross Settlement will be both left out of the liquidity metrics as they run independently of the LVPS without creating daily exposures.

Whilst SEPA real-time settlement is still subject to the Bank’s input, IPs will be operating outside normal business hours; the current Intraday throughput takes into consideration the standard day window going from 8:00 to 18:00; whilst banks should now get familiar with measuring liquidity on a 24-hour basis.

The ISO20022 migration facilitates the management of data since a single format (both for payments and for SCT/SCT-Inst) will ensure standardisation across the individual infrastructures. However, the key activities will be focused on implementing fully automated processes and integration supported by a robust infrastructure, (especially for re-balancing liquidity, alerting, and managing payments outflows). Investments should focus on expanding the data repository capacity and on interfacing each system to gather the data going in and out on a real-time basis and displaying it on user-friendly dashboards.

Re-designing the technology strategy will definitely play a key role as well as working together with the Risk Department to assess how payment behaviour will change from an intraday to a 24/7 perspective. With timed obligations and retail payments soon to be out of the LVPS picture, we will be seeing a gradual evolution of both Treasury and Risk, where liquidity will no longer be a monitoring task but rather play a strategic role.

At this stage banks should consider the following as immediate priorities:

Retail payments: these will be split between ACHs and IPs. Banks need to assess the funding activities on separate technical accounts. ECB cash accounts (TIPS) will be supported by CB collateral. However, all liquidity needs to be backed by fully automated processes

Engage in open dialogue with local regulators to assess if and how to report the IP activities in their intraday liquidity metrics calculations on a stand-alone basis as well as how to include the obligations settled on technical accounts

With the imminent Consolidation coming up, considering that TIPS will become the ‘’central connector’’ for all IP CSMs, are regulators expecting separate reports for each ECB system (RTGS+CLM, T2S and TIPS)?

Skilled staff and migration of competencies. With a gradual reduction in manual activities, staff will be required to learn how to leverage new technologies such as AI/ML/Predicative Analytics, and take advantage of powerful new tools that will likely be game changers for liquidity management optimization.

The T2-T2S Consolidation project is nevertheless a challenge that will mark the beginning of new standardised practises as well as a chance to review existing technology and systems, not to be missed.

Author: Alessandra Riccardi, Business Analyst CMT of TAS

ECB discloses new plans and milestones for TARGET Services

- No milestones to reach until March 2021

- New milestones have been added (User Testing activities started, Training for user testing started, Network connectivity tests on production started, Network connectivity tests on production completed)

- Milestones not completed in 2020 will be postponed between 8 and 12 months.

- NSP selection and contract preparation to be completed by 31 March 2021

- Software development for the required adaptation changes to TARGET2 to be completed by 30 June 2021

- Testing of the internal applications to be completed by 31 August 2021

- User Testing activities to be started by 1 December 2021

- All PSPs which have joined the SCTInst scheme and are reachable in TARGET2 should also become reachable in a TIPS central bank money liquidity account, either as a participant or as a reachable party (i.e. through the account of another PSP which is a participant)

- All ACHs offering instant payment services should migrate their technical accounts from TARGET2 to TIPS.

- 6 months to confirm, review or fine-tune their NSP choice for TARGET2

- 9 months to complete TARGET2 developments and 11 months to finalise testing

- Less than 15 months to set up their TIPS central bank money liquidity account

- NSP access in Cloud

- Intraday Liquidity

- Payments transformation

- Instant payments management in the new framework

The European Payments Ecosystem – Fintech Finance Virtual Arena

Mario Mendia, TAS Group’s International Markets SVP and Raphael Barisaac, Global Head of Cash Management and Global Co-head of Trade at Unicredit, were recently invited by Fintech Finance to speak with Ali Paterson in his Virtual Arena.

The topic was the dynamic European Payments scene today, how it’s evolving, the COVID-effect on payments, how ISO20022 is set to be a game-changer, and the challenges (and opportunities) of the T2/T2S Consolidation project.

Mario Mendia offered viewers valuable insights and shared his views on the upcoming changes to the Eurosystem, where TAS Group is playing an active role in the T2/T2S Consolidation Project.

In case you missed the Fintech Finace Virtual Arena discussion on the European Payments Ecosystem, you can watch it on our YouTube channel.

Beyond Target2 / T2S Consolidation

Need some expert help with ECMS or T2/T2S Consolidation? Get in touch

The new ECMS is coming – now is the time to act

TAS Group has been closely following the developments of the new Eurosystem Collateral Management System (ECMS) as it has been doing for the T2 / T2S Consolidation milestone, and is actively helping banks to prepare, especially in managing collateral and treasury funding.

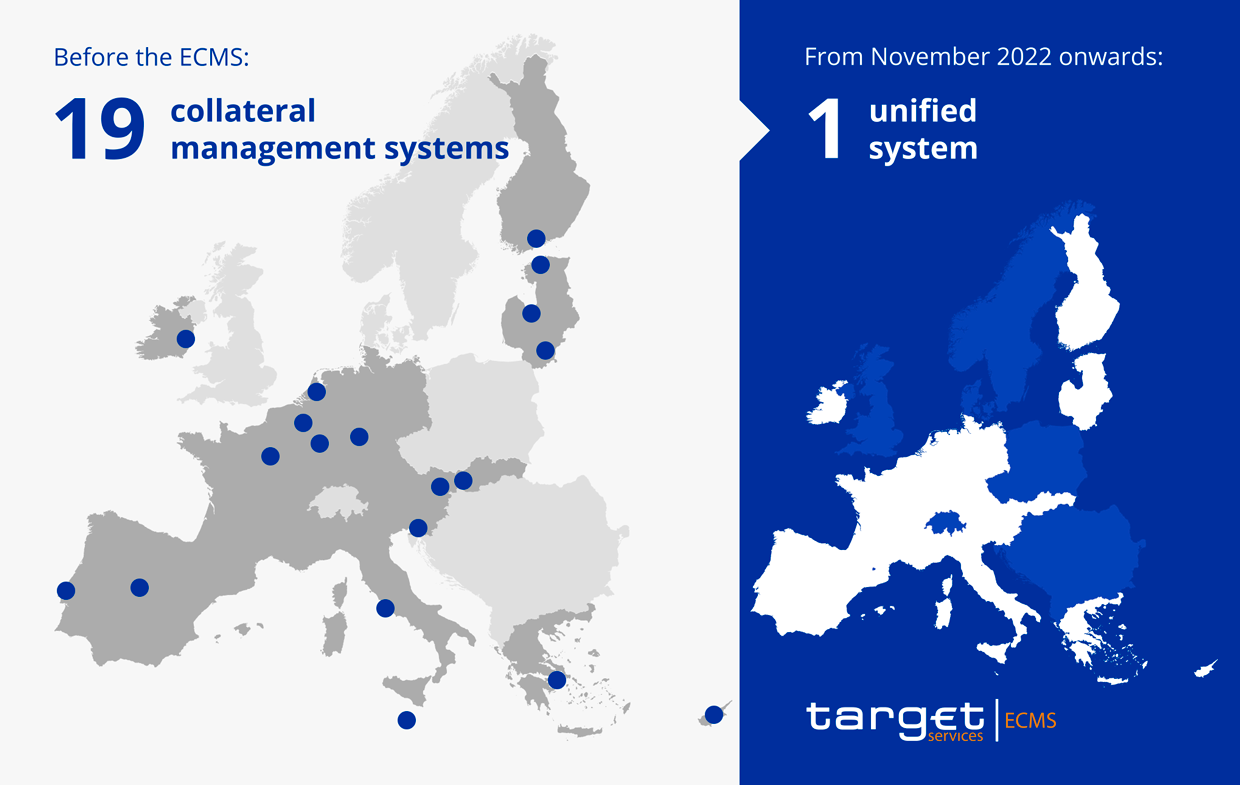

The ECMS, scheduled to go live in November 2022, will replace the existing individual systems of the 19 national central banks that are currently managing assets used as collateral for Eurosystem credit operations.

Our Aquarius Liquidity Management platform already manages the Central Bank’s Pooling Account and will guarantee in the future all the features currently being specified for the ECMS, in synergy with the liquidity management and securities settlement functions already covered by the solution.

Follow us to stay updated on the collaborative path led by TAS Group in partnership with Accenture and KPMGNeed some expert help with ECMS or T2/T2S Consolidation? Get in touch

Over 12 banks have selected TAS Group solutions to prepare for the T2/T2S Consolidation Project

Contact us

Get in touch to discover how we can help in achieving your business goals